August Mortgage Trends: A Savvy Homebuyer’s Roadmap

August has brought a welcome easing in mortgage rates—nothing dramatic, but enough to reset the strategy for savvy buyers and refinancers. Even small rate changes can influence your monthly burden and borrowing power, but the real win lies in timing and smart comparisons. In this refreshed guide, get a step-by-step roadmap on what that rate dip realistically means: from how to interpret it’s impact on your budget and how to pull the best quotes, to decision-drivers for locking in or floating rates. Whether you’re entering the home-buying arena or reconsidering your existing mortgage, here’s how to translate slight rate relief into meaningful financial advantage—without falling for marketing tricks or overpaying on fees.

Mortgage rates have shown a slight dip today, offering a glimmer of relief for both homebuyers and those looking to refinance. After months of fluctuating rates, the current drop, though modest, is being viewed as a welcome sign. For some, this could be the perfect moment to lock in a rate before the market shifts again.

In this in-depth article, we will explore:

- The latest mortgage rate figures

- How today’s rates compare to recent highs

- The reasons behind the decline

- The potential short- and long-term impact

- Actionable tips for borrowers in both the U.S. and India

By the end, you’ll have a clear picture of what this rate movement means for you and whether you should act now.

1. The Latest Mortgage Rate Data – August 9, 2025

United States

- 30-Year Fixed Mortgage Rate:

Now stands between 6.58% and 6.63%, down from around 6.72% last week. This marks the lowest level since April 2025. - 15-Year Fixed Mortgage Rate:

Averaging 5.68%, down from around 6.31% earlier this year. - Short-Term (5/1 ARM) Rates:

Hovering near 6.05%, offering an attractive option for those planning to sell or refinance within a few years.

MCLR-Linked Loans:

HDFC Bank recently reduced its Marginal Cost of Lending Rate (MCLR) by up to 5 basis points, which will slightly reduce EMIs for floating-rate borrowers..

Home Loan Interest Rates:

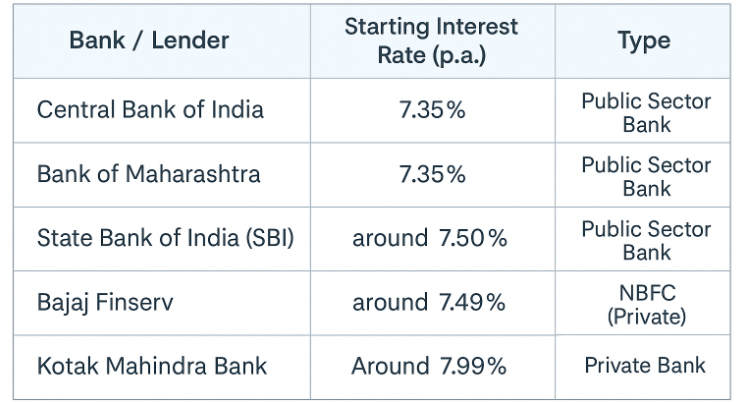

Many public sector and private banks are offering starting rates from 7.35% p.a. onwards.

Home Loan Interest Rates (Current Starting Rates)

| Bank / Lender | Starting Interest Rate (p.a.) | Type |

|---|---|---|

| Central Bank of India | 7.35% | Public Sector Bank |

| Bank of Maharashtra | 7.35% | Public Sector Bank |

| State Bank of India (SBI) | ~7.50% | Public Sector Bank |

| Bajaj Finserv | ~7.49% | NBFC (Private) |

| Kotak Mahindra Bank | ~7.99% | Private Bank |

Observations

- Public sector banks currently offer some of the most competitive rates starting from 7.35%, ideal for first-time buyers looking for predictable repayment.

- Private and NBFC lenders may have slightly higher rates but offer advantages like faster loan processing, flexible repayment, and personalized loan structures.

- The Indian mortgage market is competitive, and small reductions like the recent MCLR cut can be a good opportunity for borrowers to compare offers and consider refinancing.

Also vist:- US-India Trade War 2025: Impact, Reactions, and What Lies Ahead

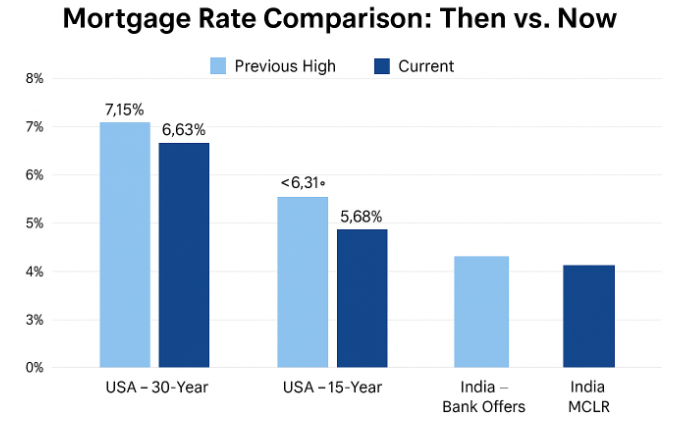

Then vs. Now – How Much Have Rates Dropped?

| Market | Previous High (Recent Months) | Current Rate | Drop |

|---|---|---|---|

| USA – 30-Year | 7.15% (2 months ago) | 6.58–6.63% | ~0.5–0.6% |

| USA – 15-Year | ~6.31% | 5.68% | ~0.6% |

| India – Bank Offers | N/A (varies) | 7.35% onwards | N/A |

| India – MCLR | — | Down by 5 bps | Small |

While the drop may seem small in percentage terms, the real-world savings over a long mortgage term can be significant—often amounting to thousands of dollars or lakhs of rupees over the loan’s life.

3. What Exactly Are Mortgage Rates?

In simple terms, a mortgage rate is the interest rate charged by a lender for a home loan.

- Fixed-Rate Mortgage:

The interest rate remains constant throughout the loan term (e.g., 15 or 30 years), offering payment stability. - Floating/Variable-Rate Mortgage:

The rate can change periodically, depending on benchmark rates like the RBI’s repo rate in India or the U.S. Federal Reserve’s policy rates. - Why They Matter:

Even a 0.25% change can make a noticeable difference in your monthly payment and the total interest paid over the years.

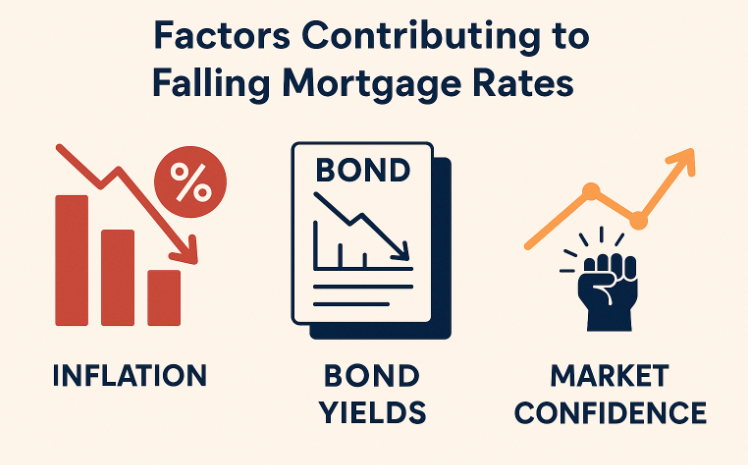

4. Why Are Mortgage Rates Falling Today?

Several factors are contributing to today’s decline in mortgage rates:

- Cooling Inflation:

With inflation showing signs of slowing, central banks are less aggressive in raising benchmark rates. - Bond Market Movements:

Mortgage rates often follow the yield on 10-year government bonds. A dip in yields tends to push mortgage rates down. - Market Confidence:

A steadier economic outlook and improving housing inventory can lower risk premiums for lenders. - Bank-Level Adjustments:

In India, marginal changes in MCLR or RLLR by banks can lead to slight reductions in retail loan rates.

5. Impact of the Drop – Who Benefits the Most?

In the United States

- Homebuyers:

Lower rates improve affordability, making monthly payments more manageable. - Refinancers:

Homeowners with older, higher-rate loans can reduce monthly payments and total interest by refinancing. - Housing Market:

Lower rates can temporarily boost demand, potentially stabilizing home prices.

In India

- Existing Floating Loan Holders:

A small MCLR drop translates into slightly lower EMIs. - New Borrowers:

Competitive fixed-rate offers can lock in lower rates for the long term. - Real Estate Developers:

Improved affordability can help revive buyer interest in slow-moving projects.

6. Is This Drop Sustainable?

Economists are cautious. While the current downward trend is encouraging, several risks remain:

- Potential Inflation Resurgence:

Any spike in inflation could force central banks to resume rate hikes. - Global Economic Uncertainty:

Trade tensions, energy prices, and geopolitical events can quickly reverse trends. - Housing Supply vs. Demand:

In the U.S., more inventory is coming online, but if rates spike, demand could falter again.

7. Action Plan for Borrowers

If You’re in the U.S.:

- Lock in a fixed rate if it’s within your budget.

- Consider refinancing if you have a loan above 7%.

- Compare lenders—small differences can save thousands.

If You’re in India:

- Review your loan type (fixed vs. floating).

- If floating, check whether the recent MCLR change affects your EMI.

- Negotiate with your lender or explore balance transfer options.

The news that mortgage rates fall today is more than just a financial headline—it’s a potential opportunity for borrowers worldwide. Whether you are in the U.S. or India, a small rate drop can have a big impact on affordability, savings, and long-term financial planning.

For now, the drop is modest, but in an environment where every basis point counts, being informed and ready to act can make all the difference. Keep an eye on market trends, and if the numbers work in your favor, this could be the moment to secure a better deal on your home loan.

FAQs: Understanding the Impact When Mortgage Rates Fall

1. What does it mean when mortgage rates fall?

When Mortgage Rates Fall, it simply means the interest charged on home loans decreases compared to previous levels. This reduction can be for fixed-rate or floating-rate mortgages. Even a small drop, such as 0.25%, can make a noticeable difference in monthly repayments and the total cost of the loan. For example, in August 2025, U.S. 30-year fixed mortgage rates fell to around 6.58%–6.63% from last week’s 6.72%. In India, certain banks reduced rates starting at 7.35% p.a., making home loans more affordable.

2. Why do mortgage rates fall?

Mortgage Rates Fall due to several economic and market-driven factors:

- Cooling inflation: Central banks slow down rate hikes.

- Bond yield changes: Lower 10-year government bond yields often push mortgage rates down.

- Market confidence: Improved housing inventory and stable economic outlook reduce risk premiums.

- Bank-level adjustments: In India, MCLR and RLLR tweaks by banks directly impact lending rates.

When these factors align, mortgage rates drop temporarily or for extended periods.

3. How does it affect homebuyers when mortgage rates fall?

When Mortgage Rates Fall, homebuyers benefit because lower interest rates make monthly payments smaller. This improves affordability, enabling buyers to purchase higher-value homes within the same budget. For example, a 0.5% drop in rates can save thousands of dollars or lakhs of rupees over the life of the loan. It also means more buyers enter the market, boosting housing demand.

4. Is it a good time to refinance when mortgage rates fall?

Yes, when Mortgage Rates Fall, it is often the best time for homeowners with higher-rate loans to refinance. Refinancing at a lower rate reduces monthly payments and overall interest costs. However, borrowers should compare the cost of refinancing (processing fees, closing costs) against the potential savings to ensure it’s worth it.

5. How much do mortgage rates need to fall to make a difference?

Even a 0.25%–0.5% drop can have a significant impact over the life of a mortgage. When Mortgage Rates Fall by half a percent, borrowers can save a large sum in interest payments over 15 or 30 years. The bigger the loan amount and the longer the term, the greater the impact of a small rate drop.

6. Do mortgage rates fall in both the U.S. and India at the same time?

Not always. While global factors like inflation trends and economic slowdowns can influence rates in both countries, local policies and central bank actions differ. For example, in August 2025, Mortgage Rates Fall occurred in both markets due to easing inflation and lower bond yields in the U.S., while in India, marginal cuts in MCLR by banks led to reduced EMIs for floating-rate borrowers.

7. Can mortgage rates fall further in 2025?

Experts believe Mortgage Rates Fall could continue if inflation remains low, bond yields drop further, and economic stability improves. However, risks like inflation resurgence, global trade tensions, or energy price spikes could reverse the trend. Borrowers should be ready to act quickly if rates drop further, as markets can change fast.

8. What should I do immediately when mortgage rates fall?

When Mortgage Rates Fall, consider these steps:

- If you’re house hunting, lock in the lower rate with your lender.

- If you have a mortgage above current rates, explore refinancing options.

- Compare lenders for the best deals—small differences save big money.

- For floating-rate borrowers, check with your bank if the drop impacts your EMI.

9. How do falling mortgage rates impact the housing market?

When Mortgage Rates Fall, buyer confidence increases, leading to more property sales. In the short term, demand rises, which can stabilize or slightly increase housing prices. In India, developers benefit as affordability improves, helping sell slow-moving projects. In the U.S., inventory moves faster, but if rates climb back up, demand could cool again.

10. Are there risks in waiting for mortgage rates to fall further?

Yes. While it’s tempting to wait for an even bigger drop, mortgage rates are unpredictable. If you wait too long, rates could rise again, costing you more in the long run. Many experts advise acting when Mortgage Rates Fall to a level that meets your affordability target rather than trying to time the absolute lowest point.

Why ‘Tricolor’ Is Trending Across the USA Right Now

Mortgage Interest Rates Drop to 6.27%: Why the Fed’s Rate Cut Isn’t Working Magic (Yet)